Context:

India’s dairy sector is not just large—it is the largest globally. India is the world’s biggest producer and consumer of dairy, accounting for nearly a quarter of global milk production. The sector is valued at ~₹10.8 trillion (~US$121 billion) as of FY25, underscoring its critical role in the country’s food economy.

Over the last five years, the Indian dairy market has demonstrated robust growth, expanding at a ~9.7% CAGR from FY20 to reach ~₹10.8 trillion in FY25. Looking ahead, the market is projected to grow at a ~10.4% CAGR from FY25 to ~₹17.7 trillion by FY30.

The dairy sector can broadly be segmented into liquid milk and value-added products such as paneer, curd, cheese, butter, ghee, khoa, skimmed milk powder, milkshakes, ice cream, yogurt, and whey. While liquid milk grew at a CAGR of ~7.2% during FY20–FY25, VAP expanded at a much faster pace of ~13.7% over the same period. This divergence is expected to widen further—between FY25 and FY30, liquid milk is projected to grow at ~5.9%, whereas VAP is expected to grow at ~15.5% making VAP VIP in dairy. This article aims to cover “Why is VAP VIP in Dairy”

Source: Milky Mist DRHP and IBEF

VAP can be further split into two sections, traditional VAP and new age / emerging VAP.

- Traditional VAP like Ghee, curd, butter, panner, buttermilk etc. and

- New Age VAP like ice cream, cheese, whey & whey products, yogurt & flavoured yogurt etc. it can be visualised as follows:

*Traditional VAP and New Age VAP have different components/products in different reports, the above table is basis Investec’s dairy report.

While traditional VAP continue to dominate the category—ghee alone accounted for ~40.8% of VAP in FY25, followed by paneer at ~21.1%—new-age VAP, despite a smaller base, have grown at a meaningfully faster pace during FY20–FY25 and are expected to continue outpacing traditional VAP going forward.

Liquid milk, while foundational to the dairy ecosystem, remains largely commoditised, with growth driven primarily by replacement—shifting from unorganised supply to cooperatives, then to branded players, and increasingly toward premium and organic variants. In contrast, VAP is creating incremental consumption and new use cases, enabling structurally higher growth (drivers discussed later in the article).

This structural shift is also evident globally as well, where value-added products account for ~75% of the dairy market. In comparison, India’s VAP mix stood at ~43% in FY25, highlighting a substantial and underpenetrated growth opportunity ahead.

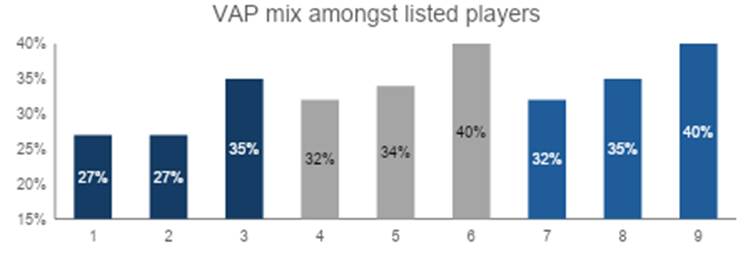

These trends are reflected in the major listed players as well:

VAP mix for all these players have increased to ~35-40% over the years and this has led to their margins increasing as well (ranging from 1.5-3%) owing to the better mix towards high margin dairy products.

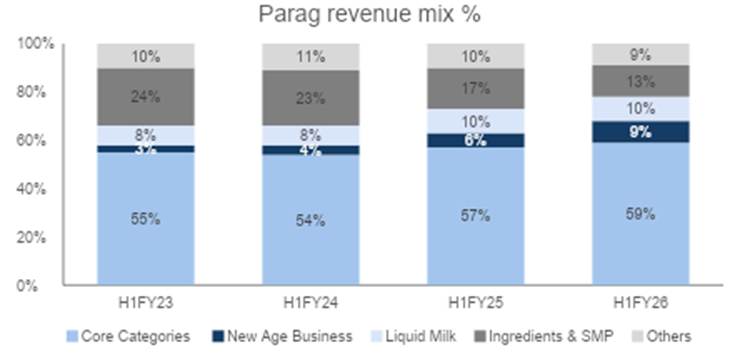

For Parag also, while VAP mix was always on the higher side >70%, it is now focusing on the “New Age” which further enhances their growth and margins:

Core Categories: Ghee, Paneer, Cheese etc.

New Age: Protein products, artisanal cheese, Organic Milk etc.

Others: Flavoured milk, Curd, etc.

While most listed dairy players have already scaled value-added products (VAP) to ~35–40%+ of their overall mix, the growth runway remains significant. This is evident from the continued capacity additions being planned across VAP categories. According to CRISIL, ~60% of the total capital expenditure projected for the dairy sector is being allocated to VAP, reinforcing that these products are no longer merely an adjacency but are central to the future growth trajectory of India’s dairy industry.

Why are companies shifting to VAP:

- Diversification of products, higher Margins and pricing power:

A diversified product portfolio provides companies with greater flexibility, and VAP offers multiple avenues for expansion, with 10+ product categories that companies can enter and experiment with.

In addition, VAP supports margin expansion through higher-value offerings. Raw milk operates on thin margins (5–10%), VADPs command margins up to 35-40%. Milk, in its raw form, is a commodity – highly perishable, undifferentiated, and heavily dependent on volatile procurement prices, leaving little room for pricing power. In contrast, turning milk into cheese, ghee, curd, yogurt, paneer, whey protein, ice creams, and flavoured beverages involves specialized manufacturing, pasteurization and fermentation technologies, flavouring, and functional enrichment (such as added protein or probiotics). Each of these steps transforms a low-margin commodity into a differentiated, branded SKU with a superior shelf-life, consumer stickiness, and higher willingness to pay.

This structural value creation also allows companies to hedge against raw milk price fluctuations, since VAP pricing is far less elastic than liquid milk. It’s precisely why legacy cooperatives like Amul and Mother Dairy have also aggressively expanded into high-margin categories.

Below is a graph showing the margin profile of VAP products. Products like ice cream (~35%), cheese, whey protein, and yogurt sit at the top end due to strong premiumisation and brand play. Ghee and butter offer mid-tier margins, while mass products such as buttermilk and lassi operate at the lower end given their limited pricing power. Liquid Milk operates at the least margins which makes it understandable why every player is jumping onto the VAP bandwagon.

Source: Milky Mist DRHP

- Longer shelf life – can manage demand and supply:

India’s dairy sector is highly seasonal, with milk production peaking in winter due to stronger lactation yields, while demand rises sharply in summer as consumers prefer products like lassi, buttermilk, yogurt, and ice cream creating winter gluts and summer shortages. Liquid milk’s ultra-short shelf life makes large-scale storage impractical, but converting surplus milk into value-added products (VAP) extends shelf life significantly (ghee and butter 180–365 days; paneer 4–6 weeks), enabling batch production, efficient storage, and wider distribution. High-demand summer products such as ice cream and yogurt can be pre-produced from winter surplus, while skimmed milk powder (SMP) acts as a low-cost bufferduring lean periods. This VAP-led approach reduces wastage, improves plant utilisation, and smooths supply-demand volatility across the year.

- Wider reach:

The Indian liquid milk industry is regionally dominated due to daily demand, short shelf life, and the need for complex cold-chain logistics for long-distance transportation. These factors, combined with low profit margins, make it economically unviable to transport liquid milk across vast distances. Additionally, the complexities involved in manufacturing, processing, maintaining cold chains, and building procurement networks—along with the time required to gain farmer trust—mean that most players establish strong regional operations before expanding further.

In contrast, VAP, with longer shelf lives and higher margins, can be developed into pan-India brands, as they can be transported more efficiently over longer distances through cold-chain logistics, enabling broader national distribution. For example, Milky Mist services 22 states and 5 UTs from a single integrated manufacturing facility, an approach that would not work for liquid milk.

- Re-rating the Dairy Business Through Value-Added Products:

A key strategic driver behind dairy companies’ push into value-added products is the significant valuation gap between dairy and FMCG businesses (while having various similar characteristics such as large market, daily consumption, distribution led models etc.). Currently, Indian dairy companies trade at EV/EBITDA multiples of ~13–20x, while FMCG (food) companies are valued at 30x+ EV/EBITDA. This valuation gap largely stems from the high share of liquid milk in dairy revenues—an inherently low-margin, low-shelf-life, price-sensitive, and largely commoditized product.

In contrast, FMCG food companies benefit from higher shelf life, superior margins, and strong brand-led differentiation, which results in more stable revenues and greater pricing power.

Value-added products (VAP) enable dairy companies to move closer to this FMCG profile. By increasing the share of VAP in their portfolios, dairy brands can improve margins, enhance revenue stability, and build stronger brands—potentially narrowing the valuation gap and, over time, approaching FMCG-like valuation multiples.

Why Now:

- Rising preferences for packaged food products:

India’s packaged food market is undergoing a structural shift driven by changing consumer lifestyles. The category has expanded from ~₹8.7 trillion in FY20 to ~₹14.2 trillion in FY25 (10.3% CAGR) and is expected to reach ~₹23.6 trillion by FY30, growing at ~10.7% CAGR. Within this, milk and milk-based value-added products (VAP) form the largest segment, accounting for ~76% of the overall market.

This growth is underpinned by a rising working population (from ~61% in FY20 to ~65% in FY25 and projected to ~69% by FY30), particularly increased female workforce participation. As time-constrained households prioritise convenience, consumption of dairy staples such as ghee, paneer, curd, and buttermilk has steadily shifted from home preparation to packaged formats, creating a durable, long-term tailwind for the milk-based VAP segment.

- Increase in disposable income:

India’s GDP per capita has risen from ~US$1,400 in 2013 to ~US$2,700 in 2024, translating to a ~6.5% CAGR, and is expected to reach ~US$4,000 by 2030 at a ~7% CAGR. This sustained income growth has meaningfully expanded disposable incomes across a large section of the population, enabling consumption beyond necessities.

Milk has historically been a non-discretionary spend, a first order of purchase for Indian households, with rising spending power, consumption is now trading up from commoditised milk to value-added dairy products (VAP). This affordability-led shift represents a structural tailwind for the VAP category—one that was largely absent a decade ago.

- Rising health and nutrition awareness:

Protein is a critical macronutrient essential for overall health, supporting muscle development, tissue repair, immune function, and metabolic processes. However, nearly 80% of India’s population consumes less than the recommended daily protein intake, with current consumption estimated at only ~65–75% of the recommended ~1.0g/kg of body weight. India’s per-capita daily protein intake of ~60–70g also remains materially lower than the 100g+ consumed in developed markets.

This deficit is compounded by poor protein quality, as cereals such as rice and wheat account for ~50% of total protein intake despite inferior amino acid profiles and low digestibility. In this context, dairy emerges as a critical source of high-quality, complete protein for India’s largely vegetarian population. Milk, yogurt, cheese, and value-added dairy products offer easily digestible protein along with essential micronutrients such as calcium, vitamin D, and potassium, positioning dairy as structurally advantaged in addressing India’s long-term protein deficiency.

- Innovative products, better quality and premiumisation:

Rising disposable incomes are driving a clear shift in consumer preferences toward premium and gourmet food products, with consumers increasingly willing to pay for superior quality, differentiation, and innovation. In response, brands are expanding into higher-indulgence offerings such as flavoured milk, flavoured yogurts, novel ice-cream variants, and artisanal cheeses.

Simultaneously, there is growing preference for higher-quality and perceived-healthier products, including organic paneer, A2 ghee, and A2 milk. Together, these trends are accelerating premiumisation within dairy and driving incremental demand for value-added products (VAP).

- Improvement in technology:

India’s dairy sector is highly fragmented, with much milk sourced from small farmers, and limited infrastructure historically caused inconsistent quality and yields. Companies are increasingly using technology-driven quality checks and procurement standardisation, e.g., Country Delight (70+ tests), Sid’s Farm (cattle management), and Akshayakalpa (integrated farm and fodder management)—to ensure consistent inputs.

Simultaneously, advances in processing and supply-chain technologies, including automated manufacturing, improved cold chains, and superior packaging, have boosted quality and shelf life of value-added dairy products. Automation enhances hygiene, consistency, and scalability in products like paneer, curd, and skimmed milk powder, while better packing (aseptic, multi-layer, and portion-controlled packaging) reduces contamination and extends freshness.

- Improved distribution:

Improved cold-storage infrastructure across retail outlets, along with more efficient cold-chain logistics, has materially enhanced shelf life while enabling faster and wider distribution of dairy products. This has helped dairy companies expand reach without compromising product quality.

In parallel, the accelerated growth of quick commerce and rapid-delivery platforms has provided a significant demand-side tailwind for the dairy industry. Dairy products account for ~30% of daily orders in the quick-commerce ecosystem, underscoring strong consumer demand. Further, according to Dr. Meenesh Shah, Chairman and Managing Director of NDDB, “quick commerce currently contributes ~4–5% of total sales for milk cooperatives—a share that is expected to increase with rising urbanisation.” New brands are heavily dependent on Quick commerce, where in for many new brands in the dairy space quick commerce accounts for more than 30% of their revenues.

- Heat waves and longer summer:

Rising temperatures and longer summers in India are structurally boosting demand for value-added dairy products (VAP). Climate trends show that cumulative heat wave exposure rising from about ~177 days in 2010 to over ~530 days by 2024—an increase of more than 200% across regions during peak summer months. Heat waves, typically from March to June and increasingly into July, are becoming more frequent and intense due to climate change and urban heat effects. This drives higher demand for cooling and hydration-oriented dairy products—such as ice cream, buttermilk, lassi, and flavoured milk—while longer, harsher summers expand the consumption window, boosting sales and adoption of VAP across urban and semi-urban markets.

Challenges unique to VAP:

While VAP and liquid milk share several structural challenges—such as milk procurement costs, cold-chain requirements, and quality control/maintenance, VAP faces additional challenges that are specific to the segment, including:

- Creating a brand:

While value-added dairy products offer clear functional and quality advantages, consumer awareness and differentiation remain a challenge. A large part of the market continues to view dairy through a commoditised lens, making it difficult for brands to justify premium pricing and differentiation without sustained investment in marketing, consumer education, and brand-building. Driving trial, communicating product benefits (health, protein content, quality, provenance), and building habitual consumption require meaningful and ongoing marketing spends, which can pressure near-term margins, particularly for private players competing against well-entrenched cooperative brands.

- Capital expenses:

Value-added dairy products (VAP) require significantly higher capex compared to liquid milk. The conversion of liquid milk into VAP begins post-procurement, necessitating incremental investment in specialised processing infrastructure. Additionally, stricter temperature control requirements and longer shelf-life management demand substantial supply-chain investments—spanning in-house cold storage, refrigerated warehousing, owned or dedicated cold-chain logistics and at times even providing freezers at the end retailer’s shop. Collectively, these factors make VAP a capital-intensive business, raising the upfront investment threshold for players in the category.

- Higher Working Capital:

While value-added products (VAP) help companies balance demand and supply, they can significantly increase working capital requirements. During high-lactation periods (typically winter), companies manufacture longer shelf-life products such as ice cream and buttermilk and sell them in the summer months, when demand is strong, but milk supply is constrained. This necessitates holding inventory for 2–3 months—unlike liquid milk, which has minimal storage requirements.

If not managed carefully, the incremental working capital costs—such as warehousing, interest on borrowings, and product wastage—can outweigh the margin benefits offered by VAP.

- Infrastructure challenges:

India remains at a relatively early stage in its value-added dairy products (VAP) journey, resulting in an underdeveloped cold-chain ecosystem. The limited penetration of specialised cold-storage logistics players and inadequate availability of temperature-controlled storage at retail outlets constrain distribution, especially for products with higher sensitivity to temperature and quality. This infrastructure gap increases spoilage risk, raises logistics costs, and restricts reach beyond top-tier urban markets, thereby slowing the pace of VAP adoption and scaling for dairy companies.

Few notable startups in dairy sector:

| Startups | About | Key products | Revenue FY24 (₹ Cr) | GM% | EBITDA % | Key investors |

| Anveshan | A D2C food brand offering traditionally made, traceable everyday staples like ghee, oils, and sweeteners | Ghee and Oil | 58.2 | 40% | -9% | DSG Venture Partners |

| Akshayakalpa | India’s first certified organic dairy company focused on producing high-quality milk and dairy products through sustainable, farmer-led supply chains | Milk (>50% revenue) and VAP | 285 | 34% | -7% | A91 |

| Country Delight | A farm-to-home fresh foods brand delivering dairy, fruits, vegetables, and staples through a subscription-led model | Milk (>50% revenue) and VAP | 1322 | 36% | -20% | Temasek |

| Two Brothers | A premium D2C organic food brand centred on regenerative farming and traditional processing of staples such as ghee, flours, and oils | Ghee and Organic food staples | 98.6 (FY25) | 59% | -22% | 360One |

| NIC ice creams | A clean-label ice cream brand known for preservative-free, fruit-based ice creams made with minimal, natural ingredients | Ice creams | 206.3 | ~52% | -16% | Jungle Ventures |

| Epigamia | A modern dairy and food brand best known for popularizing Greek yogurt in India and expanding into protein-rich and indulgent dairy snacks | Yogurt and healthy dairy-based products | 180 | 46% | -3% | DSG Venture Partners |

Conclusion:

- Milk anchors volume, VAP drives growth and profitability:

India’s dairy consumption endures, but its form evolves dramatically—from liquid milk’s high-volume, low-margin dominance to VAP-led profitability. While milk anchors volumes, VAP propels growth at 15.5% CAGR (vs. milk’s 5.9%) through ₹17.7Tn market by FY30, commanding 35-40% margins via differentiation and better pricing power.

- New players need not chase milk:

Newer players / brands need not start with milk first and then add VAP, milk can be completely ignored, and a brand can focus only on VAP. Milky Mist built a ₹2,349Cr powerhouse (FY25) on VAP, proving VAP as a standalone brand engine. Further, even startups like Anveshan, Two Brothers and various ice-cream brands like NIC, Noto etc. have been able to create a name for themselves whilst ignoring liquid milk completely.

- Key products within VAP:

While value-added dairy products (VAP) are structurally higher-margin relative to liquid milk, there are certain products which stand out in VAP as well such as ice cream – delivering margins of ~30–35% versus ~15–20% for other VAP segments. The ice-cream category also benefits from strong distribution tailwinds, particularly through quick-commerce platforms, which are well suited for impulse-led, temperature-sensitive products. Additionally, ice cream is expected to grow faster than the broader VAP category, driven by premiumisation, innovation, and longer summer seasons.

Another high-margin and high-growth adjacently scalable opportunity within VAP is whey protein. Supported by low per-capita protein consumption and rising health and fitness awareness, the whey protein market remains significantly underpenetrated, offering a large white space for category creation and brand-led growth.

- A category reset, not a trend:

Legacy firms pivot (Parag’s VAP at 91%, Heritage targeting 40%), cooperatives like Amul, Nandani and Mother Dairy also focusing on VAP and introducing multiple products in the VAP category, higher capex flows expected in VAP (60% per CRISIL) clearly indicates that these aren’t trends but is a category reset and is here to stay.

- Who can win?

India’s dairy story is no longer about litres of milk sold; it is about brands, formats, and temperature-controlled supply chains. The winners will be companies that invest early in brand-building, expand aggressively into value-added products (VAP), and back this strategy with sustained capex in processing, cold-chain logistics, and a strong, scalable retail and distribution network.

In contrast, players—whether private or cooperative—who remain focused primarily on milk volumes and short-term cash generation, without making the necessary investments in branding, technology, and supply-chain capabilities, risk being structurally disadvantaged as the industry shifts toward higher-margin, branded consumption.